Why Federal Contracts Require Bonding: A Contractor's Guide

Federal contract bonding is a legally mandated financial guarantee system that protects the government, subcontractors, and suppliers when a contractor fails to perform or pay on a public construction project. Understanding why federal contracts require bonding is not optional for any construction business pursuing government work. The Miller Act and the Federal Acquisition Regulation (FAR) establish the statutory framework that makes surety bonds a non-negotiable condition of federal contract award. This guide explains the legal foundation, the three bond types, the dollar thresholds that trigger requirements, and the practical steps every contractor must take before breaking ground on a federal job.

Why federal contracts require bonding

Federal construction contracts require bonding because the government cannot be sued or have its property liened like a private owner. That single legal reality, known as sovereign immunity, creates a gap in financial protection that bonds are specifically designed to fill. Sovereign immunity prevents liens on federal property, so subcontractors and suppliers have no lien rights if a prime contractor defaults or refuses to pay.

Surety bonds step in as the legally mandated substitute. They shift financial risk of contractor default from taxpayers to surety companies, preserving public project integrity. That risk transfer is the core purpose of federal contract bonding. Taxpayers are protected from cost overruns caused by contractor failure, and the supply chain is protected from non-payment.

The Miller Act, codified at 40 U.S.C. 3131, is the statute that makes this system mandatory. It applies to every federal construction contract above $150,000. FAR Part 28 implements the Miller Act requirements and gives contracting officers the authority to enforce bond compliance throughout the contract lifecycle.

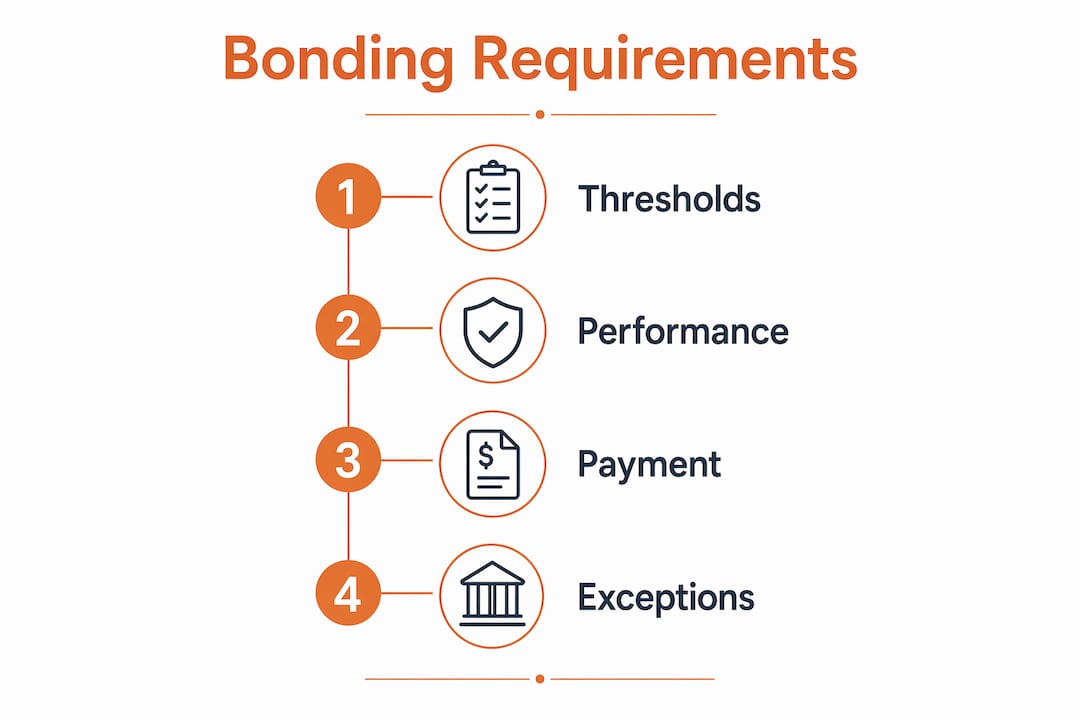

What bond types are required on federal construction contracts?

Federal construction contracts above $150,000 require three distinct bond types, each protecting a different party at a different stage of the project.

-

Bid Bond: A bid bond is typically 5–10% of the bid amount. It guarantees that the winning bidder will execute the contract and furnish the required performance and payment bonds. If the winning bidder withdraws, the bid bond compensates the government for the cost of re-soliciting the contract. This protects the government from bad-faith bids.

-

Performance Bond: A performance bond is typically set at 100% of the contract price. It guarantees that the contractor will complete the project according to the contract terms. If the contractor defaults, the surety arranges completion or compensates the government up to the bond amount. Performance bonds penalize up to the full contract value, which gives the surety a strong financial incentive to vet contractors carefully before issuing coverage.

-

Payment Bond: A payment bond is also typically set at 100% of the contract price. It guarantees that all laborers, subcontractors, and material suppliers will be paid. Payment bond claims are typically limited to first and second-tier claimants, meaning direct subcontractors and their immediate suppliers. Third-tier suppliers generally do not have Miller Act rights.

Pro Tip: Request a copy of the payment bond from the contracting officer before you mobilize. FAR 28.106-6 requires contracting officers to provide payment bond information and surety company details to subcontractors on request. Getting this information early puts you in a stronger position if payment disputes arise later.

The legal rights subcontractors gain from a payment bond are significant. Without a bond, a subcontractor on a federal job has no lien remedy and no direct claim against the government. With a bond, the subcontractor has a direct legal claim against the surety company, which is a real and enforceable financial remedy.

How does sovereign immunity change subcontractor rights on federal jobs?

The difference between a federal project and a private project comes down to one legal concept: sovereign immunity. On a private project, an unpaid subcontractor or supplier can file a mechanic’s lien against the property. That lien clouds the title and gives the claimant real leverage to force payment.

On a federal project, that option does not exist. The federal government owns the property, and sovereign immunity bars any lien against it. The table below shows how subcontractor protections differ between the two project types.

| Protection Type | Private Project | Federal Project |

|---|---|---|

| Mechanic’s Lien | Available against property | Not available; sovereign immunity applies |

| Payment Bond | Optional; lender may require | Mandatory under Miller Act above $150,000 |

| Claim Filing Venue | State court | Federal district court |

| Claim Deadline | Varies by state | Typically within 90 days of last work |

| Claimant Tiers | Varies by state law | First and second tier only under Miller Act |

The payment bond is the exclusive financial substitute for mechanic’s liens on federal projects. That is not a policy preference. It is the only legal remedy available to unpaid subcontractors and suppliers on government construction jobs. Private lenders have recognized the strength of this model. The Miller Act bond structure is now considered the gold standard in construction risk management, and many private lenders require Miller Act-style bonds even on private projects.

What are the federal statutes and thresholds governing bond requirements?

The Miller Act at 40 U.S.C. 3131 sets the primary threshold. Contracts exceeding $150,000 require both a performance bond and a payment bond, each at 100% of the contract price. That is the standard rule, and it applies to the vast majority of federal construction work.

Contracts between $35,000 and $150,000 fall into a middle tier. Full payment bonds are not required at this level, but alternative payment protections must be in place. These alternatives can include escrow arrangements or other financial instruments approved by the contracting officer. Contracts below $35,000 have no federal bonding requirement, though agencies may impose their own conditions.

| Contract Value | Performance Bond | Payment Bond | Alternative Protection |

|---|---|---|---|

| Below $35,000 | Not required | Not required | Agency discretion |

| $35,000 to $150,000 | Not required | Not required | Required |

| Above $150,000 | 100% of contract price | 100% of contract price | Not applicable |

FAR Part 28 governs how contracting officers administer these requirements. Contracting officers can reduce bond amounts when full bonding is impractical, but they cannot reduce payment bonds below the performance bond amount. That rule exists specifically to preserve subcontractor protections. Reducing the payment bond below the performance bond would leave the supply chain exposed while still protecting the government, which the FAR does not permit.

Pro Tip: When you review a federal solicitation, check FAR Clause 52.228-15 for construction contracts. That clause specifies the exact bond amounts required for your specific contract. Misreading the bond requirement is one of the most common federal bidding mistakes contractors make, and it can disqualify your bid entirely.

The surety bond involves three parties: the contractor (principal), the surety company, and the government (obligee). The surety guarantees the contractor’s obligations to the government. If the contractor defaults, the surety steps in to arrange completion or pay valid claims. Choosing a surety listed on the U.S. Department of the Treasury’s Circular 570 is mandatory for federal work. Circular 570 lists approved sureties and their underwriting limits by state.

What practical steps should contractors take regarding bonding on federal jobs?

Understanding the legal framework is necessary. Executing the right steps in the right order is what actually protects your business. Here is the sequence every contractor and subcontractor should follow on a federal construction project.

-

Verify bond requirements during the solicitation review. Read FAR Clause 52.228-15 and the solicitation’s bonding section before you price the job. Know whether the contract exceeds $150,000 and what bond amounts are required. Factor surety costs into your bid.

-

Engage a Treasury-listed surety early. Surety underwriting takes time. Your surety will review your financial statements, work-in-progress schedule, and past performance history. Starting this process after contract award creates delays that can jeopardize your contract execution timeline.

-

Request payment bond information as a subcontractor. Under FAR 28.106-6, contracting officers must provide payment bond details to subcontractors on request. Contractors often overlook requesting this information proactively, which weakens their position in payment disputes. Get the bond number, surety name, and contact information before work begins.

-

Document your work and deliveries meticulously. Miller Act claims require proof of the labor and materials you furnished. Keep dated delivery receipts, signed daily logs, and invoices organized by contract. This documentation is your evidence if you need to file a claim.

-

Track your Miller Act claim deadlines. Miller Act claims must be filed in federal district court, typically within 90 days of the last date you furnished labor or materials. Missing these deadlines results in complete forfeiture of your payment remedy. Set calendar reminders the day you mobilize.

-

Understand your tier position. First-tier subcontractors have direct Miller Act rights. Second-tier subcontractors must give written notice to the prime contractor within 90 days of last furnishing. Third-tier and below generally have no Miller Act rights. Know where you sit in the contract chain before you sign.

Understanding past performance requirements alongside bonding gives you a complete picture of what federal agencies evaluate before awarding contracts. Strong past performance records also help you qualify for better surety terms and lower bond premiums over time.

Key takeaways

Federal contracts require bonding because sovereign immunity eliminates lien rights on government property, making surety bonds the only legally enforceable financial protection for all parties in a public construction project.

| Point | Details |

|---|---|

| Sovereign immunity drives bonding | Federal property cannot be liened, so bonds are the mandatory substitute for subcontractor payment protection. |

| Miller Act sets the threshold | Contracts above $150,000 require performance and payment bonds, each at 100% of the contract price. |

| Three bond types serve distinct roles | Bid bonds protect re-solicitation costs; performance bonds cover completion; payment bonds protect the supply chain. |

| Claim deadlines are strict | Miller Act claims must typically be filed within 90 days of last work; missing the deadline forfeits all remedies. |

| Request bond info proactively | Subcontractors should obtain payment bond details from the contracting officer before work begins, not after disputes arise. |

Bonding is the foundation, not the fine print

By Rowena

After years of working with contractors entering the federal market, the pattern I see most often is this: bonding gets treated as a paperwork step rather than a risk management tool. Contractors focus on winning the bid and assume the bonding will sort itself out. That assumption costs real money.

The bond clause in your federal contract is not boilerplate. It defines your financial exposure, your surety’s obligations, and your subcontractors’ legal rights. I have seen prime contractors lose their surety relationships mid-project because they did not understand their bond’s scope, and the downstream consequences for subcontractors were severe.

My strongest advice is to build your surety relationship before you need it. A surety that knows your financials, your project history, and your management team will underwrite your bonds faster and at better rates. That relationship is a competitive asset, especially when you are bidding against contractors who treat bonding as an afterthought.

The Miller Act bond structure is also worth studying even if you primarily work private jobs. Private lenders increasingly require the same protections. Understanding federal bonding requirements positions you to work in both markets with confidence.

— Rowena

How Federal-rconstructionsolutions supports your bonding and bid compliance

Federal-rconstructionsolutions helps construction businesses meet the full range of federal procurement requirements, including bonding compliance, RFP preparation, and bid submission support. The 5551 Pillar program delivers a structured approach to federal contracting that has achieved 90% compliance rates for client bid submissions.

Whether you are preparing your first federal bid or scaling your government contracting portfolio, Federal-rconstructionsolutions provides the guidance you need to get bonding right from the start. From reviewing FAR clauses to coordinating surety documentation, the team works alongside you at every stage. Visit the federal procurement services page to learn how the 5551 Pillar program can support your next federal contract pursuit.

FAQ

What is the miller act and who does it apply to?

The Miller Act is a federal statute at 40 U.S.C. 3131 that requires performance and payment bonds on federal construction contracts exceeding $150,000. It applies to prime contractors working directly with the federal government as the project owner.

Can subcontractors file a lien on a federal construction project?

No. Sovereign immunity prevents any mechanic’s lien against federal property. The payment bond under the Miller Act is the exclusive financial remedy available to unpaid subcontractors and suppliers on federal jobs.

What happens if a contractor defaults on a federal bond?

If the contractor defaults, the surety company arranges project completion or compensates the government and valid claimants up to the bond amount. The surety then seeks reimbursement from the defaulting contractor.

How do subcontractors file a miller act payment bond claim?

Subcontractors must file their claim in federal district court, typically within 90 days of the last date they furnished labor or materials. Second-tier subcontractors must also provide written notice to the prime contractor within that same window.

Are bonds required on federal contracts below $150,000?

Contracts between $35,000 and $150,000 require alternative payment protections rather than full Miller Act bonds. Contracts below $35,000 have no federal bonding requirement, though individual agencies may set their own conditions.